Blank California 3541 PDF Form

In the world of California-based film and television production, navigating tax incentives is as crucial as casting the right lead actor. Central to this financial landscape is the California Form 3541, a beacon for qualifying productions seeking tax relief. Enacted to bolster the entertainment industry within the state, this form is a gateway to claiming the California Motion Picture and Television Production Credit. At its core, the form serves as an attachment to one's California tax return, an essential step for producers and financiers keen on maximizing their investment returns. The form outlines a variety of avenues to claim credits, from direct production expenditures to credits received through pass-through entities or even purchased and assigned credits among affiliated corporations. Detailing procedures for carryover computation and the intricate rules governing credit sale and assignment, Form 3541 encapsulates the state's commitment to keeping the silver screen shimmering in the Golden State. Exploring this form unveils the complexities and opportunities of California's tax incentive program, designed not only to entice productions to film within its borders but to understand the fiscal landscape that underpins the glitter of Hollywood.

Document Preview Example

TAXABLE YEAR |

|

CALIFORNIA MOTION |

PICTURE AND TELEVISION |

|

|

|

|

|

|

|

|

|

|

CALIFORNIA FORM |

|||||||||||||||||||||||||||

2012 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

3541 |

|

|

|||||||||||||||||||||||||||||||||||||||

|

PRODUCTION CREDIT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attach to your California tax return. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Name(s) as shown on your California tax return |

|

|

|

|

|

|

|

|

|

|

|

SSN or ITIN Corporation no. FEIN |

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CA Secretary of State (SOS) file number |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

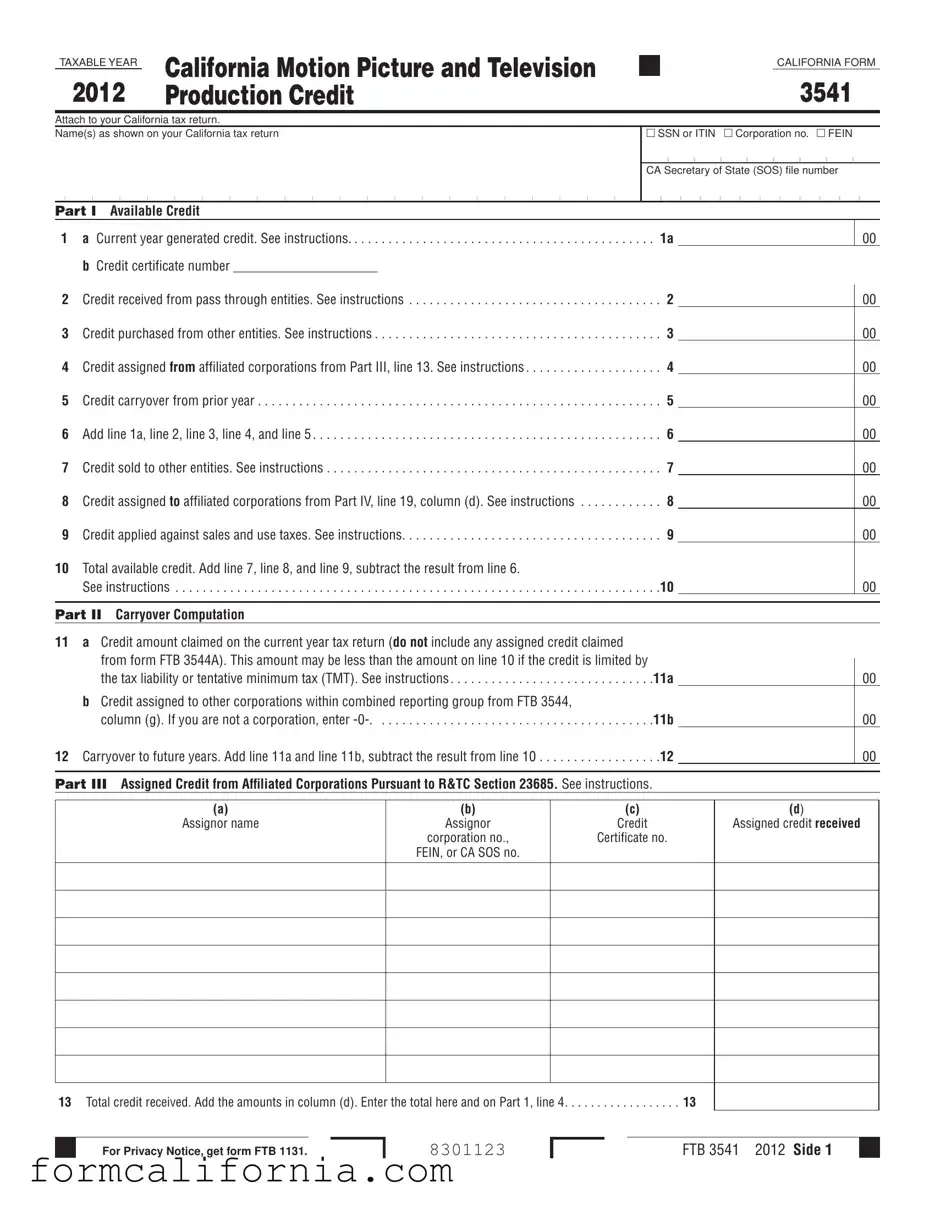

PART I Available Credit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

1 a Current year generated credit. See instructions |

1a |

bCredit certificate number _____________________

2 Credit received from pass through entities. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 3 Credit purchased from other entities. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 4 Credit assigned from affiliated corporations from Part III, line 13. See instructions . . . . . . . . . . . . . . . . . . . . 4 5 Credit carryover from prior year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 6 Add line 1a, line 2, line 3, line 4, and line 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 7 Credit sold to other entities. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 8 Credit assigned to affiliated corporations from Part IV, line 19, column (d). See instructions . . . . . . . . . . . . 8 9 Credit applied against sales and use taxes. See instructions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

10Total available credit. Add line 7, line 8, and line 9, subtract the result from line 6.

See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

PART II Carryover Computation

11a Credit amount claimed on the current year tax return (do not include any assigned credit claimed

from form FTB 3544A). This amount may be less than the amount on line 10 if the credit is limited by

the tax liability or tentative minimum tax (TMT). See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11a

bCredit assigned to other corporations within combined reporting group from FTB 3544,

column (g). If you are not a corporation, enter

12 Carryover to future years. Add line 11a and line 11b, subtract the result from line 10 . . . . . . . . . . . . . . . . . .12

PART III Assigned Credit from Affiliated Corporations Pursuant to R&TC Section 23685. See instructions.

00

00

00

00

00

00

00

00

00

00

00

00

00

(a)

Assignor name

(b)

Assignor

corporation no.,

FEIN, or CA SOS no.

(c)

Credit

Certificate no.

(d)

Assigned credit received

13 Total credit received. Add the amounts in column (d). Enter the total here and on Part 1, line 4. . . . . . . . . . . . . . . . . . 13

For Privacy Notice, get form FTB 1131.

8301123

FTB 3541 2012 Side 1

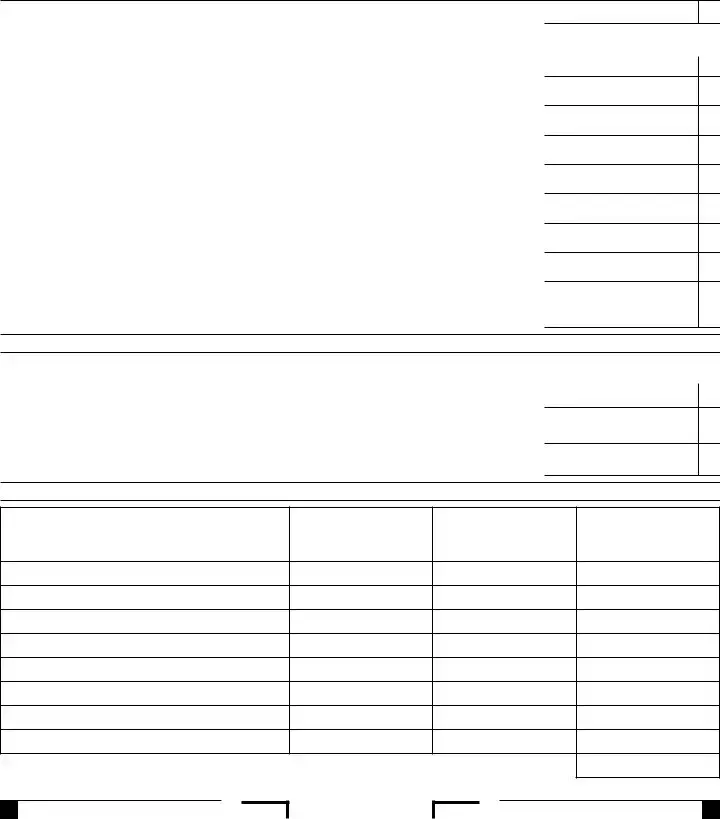

PART IV Credit Assigned to Affiliated Corporations Pursuant to R&TC Section 23685. See instructions.

14 Add line 1a and line 2 from Side 1, Part I . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

15 Tax liability. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

16Excess credit available for assigning to affiliated corporations. Subtract line 15 from line 14, enter the

result here and on line 17, column (e). If the result is ‘0’ or less, enter ‘0’. See instructions. . . . . . . . . . . . . .16 This is the maximum amount of credit that may be assigned to affiliated corporations.

00

00

00

Credit Assigned to Affiliated Corporations.

|

(a) |

(b) |

(c) |

(d) |

(e) |

|

Assignee name |

Assignee corp. no., |

Credit |

Amount of |

Credit amount available |

|

|

FEIN, or CA SOS no. |

Certificate no. |

credit assigned |

for assignment |

|

|

|

|

|

|

17 |

|

|

|

|

|

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 Add the amounts in column (d). Enter the total here and on Part I, line 8 . . . . . . . . . . . . . . . . . . . . . . . 19

Side 2 FTB 3541 2012

8302123

Instructions for Form FTB 3541

California Motion Picture and Television Production Credit

Important Information

California Motion Picture and Television Production Credit. For taxable years beginning on or after January 1, 2011, Revenue & Taxation Code (R&TC) Section 17053.85 and Section 23685 allow a qualified taxpayer a California motion picture and television production credit against the net tax (individuals) or tax (corporations) and/or qualified sales and use tax. The credit, which is allocated and certified by the California Film Commission (CFC), is 20% of expenditures attributable to a qualified motion picture or 25% of production expenditures attributable to an independent film or a television series that relocates to California.

Write “CFC Credit”– Taxpayers attaching form FTB 3541, California Motion Picture and Television Production Credit, to the tax return should write “CFC Credit” in red ink at the top margin of their tax return.

Use of Credit – The credit can be used by the qualified taxpayer to:

•Offset franchise or income tax liability. Use credit code number 223 when claiming this credit.

•Sell to an unrelated party (independent films only).

•Assign to an affiliated corporation.

•Apply against qualified sales and use taxes.

This credit is not refundable.

Sales and Use Taxes – A qualified taxpayer who has been issued a certified Form M, Tax Credit Certificate, from the CFC may make an irrevocable election with the Board of Equalization (BOE) to apply the credit against qualified sales and use taxes. For more information, go to boe.ca.gov and search for ca film.

Credit Assignment – A qualified taxpayer that is a corporation or is taxed as a corporation and whose credit exceeds the tax may elect to assign the credit to an affiliated corporation(s). The election to assign the credit is irrevocable. For more information, see General Information C, Credit Assignment.

Sale of Credit Attributable to an Independent Film – A qualified taxpayer may sell a credit, attributable to an independent film, to an unrelated party once the taxpayer receives Form M from the CFC. The credit can only be sold by the qualified taxpayer that generated the credit (that is a corporation, a Limited liability company (LLC) or partnership taxed as a corporation, or an individual) or by a shareholder, beneficiary, partner, or member who received the credit as their distributive or

Seller – A qualified taxpayer that sells an independent film credit is required to report the gain on the sale of the credit in the amount of the sale price.

Buyer – If the credit was purchased for less than the credit amount stated on Form M, the buyer is required to report income in the amount of the difference between the credit amount claimed on its return and the purchase price.

General Information

A Purpose

Use form FTB 3541 to report the credit for the production of a qualified motion picture in California that was:

•Allocated from the CFC on Form M, Tax Credit Certificate.

•Passed through from S corporations, estates and trusts, partnerships, or limited liability companies (LLCs) taxed as partnerships.

•Purchased from a qualified taxpayer.

•Assigned to or from an affiliated corporation under R&TC Section 23865(c)(1). For more information, see General Information C, Credit Assignment.

•Applied or will be applied against BOE qualified sales and use taxes. For more information, go to boe.ca.gov and search for ca film.

Note: Each entity that received or assigned a motion picture and television production credit from or to another entity within a combined reporting group must complete a separate form FTB 3541.

S corporations, estates and trusts, and partnerships, or LLCs taxed as partnerships should complete form FTB 3541 to figure the amount of credit to

Corporate taxpayers attach this form to Form 100, California Corporation Franchise or Income Tax Return, or Form 100W, California Corporation Franchise or Income Tax Return - Water’s Edge Filers.

Individual taxpayers attach this form to Form 540, California Resident Income Tax Return, or Form 540NR, California Nonresident or

B Definitions

Credit certificate. Credit certificate means the certificate issued by the CFC for the allocation of the credit to a qualified taxpayer.

Qualified taxpayer. Qualified taxpayer means a taxpayer who has paid or incurred qualified expenditures and has been issued a credit certificate by the CFC. In the case of any

Qualified motion picture. Qualified motion picture means a motion picture that is produced for distribution to the general public, regardless of medium. For more information, refer to the R&TC Section 17053.85, Section 23685, or go to film.ca.gov.

Independent film. Independent film means a motion picture with a minimum budget of one million dollars ($1,000,000) and a maximum budget of ten million dollars ($10,000,000) that is produced by a company that is not publicly traded and publicly traded companies do not own, directly or indirectly, more than 25 percent of the producing company.

Television series. Television series means a television series that relocated to California, without regard to episode length or initial media exhibition, that filmed all of its prior season or seasons outside of California and for which the taxpayer certifies that this credit is the primary reason for relocating to California.

Affiliated corporation. Affiliated corporation has the meaning provided in R&TC Section 25110(b), except that “100 percent” is substituted for “more than 50 percent” wherever it appears in the section and “voting common stock” is substituted for “voting stock” wherever it appears in the section. For more information, see General Information C, Credit Assignment.

FTB 3541 Instructions 2012 Page 1

C Credit Assignment

For taxable years beginning on or after January 1, 2011, R&TC Section 23685(c)(1) allows a qualified taxpayer to assign a California motion picture and television production credit to an eligible assignee. The credit must first exceed the tax of the qualified taxpayer (the assignor) for the taxable year in which the credit is to be assigned.

The election to assign any credit is irrevocable. The assignor shall make the election and report the credit assignment by completing Part IV, Credit Assigned to Affiliated Corporations Pursuant to R&TC Section 23685. Once a credit is assigned to an eligible assignee, it cannot be reassigned. The assignor will reduce the credit amount available for assignment by the amount of the credit assigned.

After assignment of an eligible credit, the eligible assignee may use the credit against income tax liability, or apply it against BOE qualified sales and use taxes. Also, the restrictions and limitations that applied to the assignor (entity that originally generated the credit) may apply to the eligible assignee.

There is no requirement of payment or other consideration for assignment of the credit by an eligible assignee to an assignor.

The assignor and the eligible assignee shall maintain the information necessary to substantiate any credit assigned and to verify the assignment and subsequent use of the credit assigned. Lack of substantiation may result in the disallowance of the assignment. The assignor and the eligible assignee shall each be liable for the full amount of any tax, addition to tax, or penalty that results from any disallowance of the credit assigned under R&TC Section 23685. The Franchise Tax Board may collect such amount in full from either the assignor or the eligible assignee.

Note: This credit may also be assigned under the credit assignment rules of R&TC Section 23663. Any portion of the credit assigned under either Section 23663 or 23685 may not be subsequently assigned under either statute. For more information on credit assignment under R&TC Section 23663, get form FTB 3544, Election to Assign Credit Within Combined Reporting Group, and form FTB 3544A, List of Assigned Credit Received and/or Claimed by Assignee.

Assignor. An assignor is the qualified taxpayer that receives Form M from the CFC. The following rules must be met before a credit can be assigned:

•The assignor must be taxed as a corporation.

•The credit must first exceed the “tax” of the assignor for the taxable year in which the credit is to be assigned.

•The eligible assignee must be an affiliated corporation as defined by R&TC Section 23685(c)(1).

Eligible assignee. An eligible assignee is any affiliated corporation, which includes a corporation where one of the following applies:

•Owns, directly or indirectly, 100 percent of the assignor’s voting common stock.

•The assignor owns, directly or indirectly, 100 percent of the voting common stock.

•Is wholly owned by a corporation or individual owning 100 percent of the voting common stock of the assignor, or

•Is a stapled entity as defined in R&TC Section 25105.

D Limitations

The credit cannot reduce the S corporation 1.5%

The credit cannot reduce regular tax below the tentative minimum tax. For more information, get Schedule P (100, 100W, 540, 540NR, or 541), Alternative Minimum Tax and Credit Limitations.

S corporation. If a C corporation has unused credit carryovers when it elects S corporation status, the credit carryovers may not be passed through to the S corporation or the shareholders. For more information, get Schedule C (100S), S Corporation Tax Credits.

Disregarded business entity. If a taxpayer owns an interest in a disregarded business entity [for example, a single member limited liability company (SMLLC), which for tax purposes is treated as a sole proprietorship if owned by an individual or a division if owned by a corporation], the credit amount received from the disregarded entity is limited to the difference between the taxpayer’s regular tax figured with the income of the disregarded entity, and the taxpayer’s regular tax figured without the income of the disregarded entity. If the credit is sold under Section 17053.85(c) or assigned or sold under Section 23685(c) this restriction does not apply.

E Carryover

If the available credit exceeds the current year tax liability or is limited by tentative minimum tax, the unused credit may be carried over for six years or until the credit is exhausted, whichever occurs first. Apply the credit carryover to the earliest taxable year(s) possible. In no event can the credit be carried back and applied against a prior year’s tax.

Retain all records that document this credit and carryover used in prior years. The FTB may require access to these records.

Specific Line Instructions

Part I – Available Credit

Line 1a – Current year generated credit. If you received Form M from CFC, enter the full amount of credit allocated to you by the CFC as shown on Form M. If you received more than one Form M during the taxable year, add the credit amounts from all Form Ms and enter the total on this line. If you received the credit from a pass through entity, purchased the credit from a qualified taxpayer, or received the credit through an assignment from another corporation pursuant to R&TC Section 23685, do not enter the amounts on this line. Instead, enter these amounts on line 2, line 3, or line 4, respectively.

Line 1b – Enter the credit certificate number from Form M for the current year generated credit entered on line 1a. If you reported multiple credits on line 1a, list all credit certificate numbers on this line.

Line 2 – Credit received from pass through entities. Add the

Line 3 – Credit purchased from other entities. Enter the amount of credit purchased from a qualified taxpayer. Do not enter the consideration amount paid for the credit.

Line 4 – Credit assigned from affiliated corporations. If you received an assigned credit from an affiliated corporation pursuant to R&TC Section 23685, complete Part III, Assigned Credit from Affiliated Corporations Pursuant to R&TC Section 23685, and enter the amount from Part III, line 13 on this line.

Line 7 – Credit sold to other entities. Enter the amount of credit sold to an unrelated party from form FTB 3551, box 7 (Total amount of credit being sold).

Line 8 – Credit assigned to affiliated corporations. If you assigned a credit to an affiliated corporation pursuant to R&TC Section 23685, complete Part IV, Credit Assigned to Affiliated Corporations Pursuant to R&TC Section 23685. Enter the amount from Part IV, line 19, on this line.

Line 9 – Credit applied against sales and use taxes. If you applied any portion of the credit against qualified sales and use taxes, enter the amount on this line.

Page 2 FTB 3541 Instructions 2012

Part II – Carryover Computation

Line 11a – Credit amount claimed on the current year tax return. The credit amount you can claim on your tax return may be limited. Refer to the credit instructions in your tax booklet for more information. These instructions also explain how to claim this credit on your tax return. Use credit code number 223 when you claim this credit. Also see General Information D, Limitations.

Line 11b – Credit assigned to other corporations within combined reporting group. If you assigned a credit to an affiliated corporation pursuant to R&TC Section 23663, enter the total credit assigned from form FTB 3544, column (g) on this line.

Part III – Assigned Credit from Affiliated Corporations Pursuant to R&TC Section 23685.

Complete this table if you received credits assigned from an affiliated corporation pursuant to R&TC Section 23685.

Column (a) – Assignor name. Enter the name of the corporation that assigned the credit.

Column (b) – Assignor corporation number , FEIN, or CA SOS number. Enter the California corporation number, FEIN, or CA SOS number of the corporation that assigned the credit.

Column (c) – Credit Certificate number. Enter the credit certificate number from the qualified taxpayer’s (assignor’s) tax credit certificate issued by the CFC.

Column (d) – Assigned credit received. Enter the assigned credit received from the assignor.

Part IV – Credit Assigned to Affiliated Corporations Pursuant to R&TC Section 23685.

Line 15 – Tax liability. Enter on this line the amount from Form 100, California Corporation Franchise or Income Tax Return, or Form 100W, California Corporation Franchise or Income Tax Return —

Line 16 – Excess credit available for assigning to affiliated corporations. Subtract line 15 from line 14. If the result is:

•‘0’ or less, enter ‘0’. Do not complete the Credit Assigned to Affiliated Corporations table. You do not have available credit to assign.

•More than zero, this is the maximum amount of credit that may be assigned to affiliated corporations. Enter the amount on Line 17, column (e).

Complete the Credit Assigned to Affiliated Corporations table under Part IV if you have a balance on line 16 and will assign credits to affiliated corporations pursuant to R&TC Section 23685.

The following instructions are for completing line 18:

Column (a) – Assignee name. Enter the name of the corporation that is receiving a credit assignment from the assignor.

Column (b) – Assignee California corporation number, FEIN, or CA SOS number. Enter the California corporation number, FEIN, or CA SOS number of the corporation that is receiving the credit assignment. If the corporation has applied for but not yet received the California corporation number or FEIN, enter “Applied For” in column (b). If

the corporation is a

Column (c) – Credit Certificate number. Enter the credit certificate number from Form M issued to you by the CFC.

Column (d) – Amount of credit assigned. Enter the amount of credit that is being assigned to an assignee.

Column (e) – Credit Amount available for assignment. Subtract the amount in column (d) from the amount in previous line column (e).

FTB 3541 Instructions 2012 Page 3

Document Specs

| Fact | Detail |

|---|---|

| Governing Law | Revenue & Taxation Code (R&TC) Section 17053.85 and Section 23685 |

| Form Purpose | To report the California Motion Picture and Television Production Credit |

| Credit Types | 20% for qualified motion pictures, 25% for independent films or TV series relocating to California |

| Allocation Authority | California Film Commission (CFC) |

| Credit Usage | Offset tax liability, sale to unrelated parties (independent films only), assign to affiliated corporations, or apply against sales and use taxes |

| Assignment and Sale | Credit can be sold by or assigned from the qualifying taxpayer to affiliated corporations or eligible assignees, but such an assignment is irrevocable |

Detailed Instructions for Writing California 3541

Filling out the California Form 3541 for the Motion Picture and Television Production Credit is pivotal for qualified taxpayers who aim to claim credits related to the production of a qualified motion picture in California. This process involves providing detailed information about available credits, carryover computations, and credit assignments to or from affiliated corporations. Following a systematic approach to complete this form ensures accuracy and compliance with the California Revenue and Taxation Code.

- Begin by entering the Taxable Year at the top of the form.

- Include Name(s) as shown on your California tax return followed by your SSN or ITIN, Corporation no., or FEIN, and CA Secretary of State (SOS) file number if applicable.

- In Part I - Available Credit, start with line 1a by specifying the Current year generated credit based on the instructions and include the Credit certificate number.

- For line 2, enter any Credit received from pass-through entities, and on line 3, note any Credit purchased from other entities.

- On line 4, detail any Credit assigned from affiliated corporations, and if you have any Credit carryover from the prior year, record this on line 5.

- Sum up the amounts from lines 1a through 5 and enter the total on line 6.

- Identify any Credit sold to other entities on line 7, Credit assigned to affiliated corporations on line 8, and Credit applied against sales and use taxes on line 9.

- Calculate your Total available credit by adding lines 7, 8, and 9, then subtracting the result from line 6. Enter this on line 10.

Part II - Carryover Computation requires you to specify the Credit amount claimed on the current year tax return on line 11a and any Credit assigned to other corporations within the combined reporting group on line 11b. Then, calculate your Carryover to future years and enter this on line 12.

- In Part III - Assigned Credit from Affiliated Corporations, provide details of any assigned credit received including the assignor's name, number, credit certificate number, and the assigned credit received on line 13.

- For Part IV - Credit Assigned to Affiliated Corporations, document any credit you are assigning to affiliated corporations, including relevant names, numbers, and the amount of credit assigned. This section's completion affects the totals reported in previous parts of the form.

- Ensure all information is correct and complete before attaching the form to your California tax return.

After completing and attaching Form 3541 to your tax return, remember to review the entire return for accuracy. Given the complexities associated with tax credits and the potential impact on your tax liabilities, it's essential to ensure all information is correct to maximize your entitlements and comply with state taxation laws.

Things to Know About This Form

What is the California 3541 form used for?

The California 3541 form is designed for reporting the California Motion Picture and Television Production Credit. This credit is aimed at qualified taxpayers who have incurred eligible expenses for the production of a qualified motion picture in California. Taxpayers can attach this form to their California tax return to claim the credit against their net tax (for individuals) or tax (for corporations), or against qualified sales and use taxes. Additionally, credits can be sold to unrelated parties, assigned to affiliated corporations, or purchased from other entities.

Who qualifies for the California Motion Picture and Television Production Credit?

Qualification for the California Motion Picture and Television Production Credit is granted to taxpayers who have paid or incurred qualified expenditures for the production of a qualified motion picture in California and have been issued a credit certificate by the California Film Commission (CFC). Eligibility also extends to taxpayers who have received credits through pass-through entities, purchased credits from qualified taxpayers, or acquired credits through assignments from affiliated corporations.

How can the credit be utilized?

The California Motion Picture and Television Production Credit can be utilized in multiple ways:

- To offset franchise or income tax liability directly.

- By selling the credit to an unrelated party, but this is exclusively available for independent films.

- Through assigning the credit to an affiliated corporation.

- By applying the credit against qualified sales and use taxes. A certified Form M from the CFC is necessary for this option, and specific election must be made with the Board of Equalization (BOE).

Note that this credit is non-refundable.

What are the key definitions relevant to the California 3541 form?

Several key terms are essential for understanding the California 3541 form:

- Credit Certificate: The certificate issued by the CFC that allocates the credit to a qualified taxpayer.

- Qualified Taxpayer: A taxpayer eligible for the credit based on specified criteria, including the payment or incurrence of qualified expenditures.

- Qualified Motion Picture: This refers to a motion picture produced for distribution to the general public, which meets the eligibility criteria set forth by the CFC.

- Affiliated Corporation: As defined in the Revenue & Taxation Code, an affiliated corporation is related in a manner that meets specific ownership criteria.

Can the credit be carried over to future years?

Yes, if the available credit exceeds the current year tax liability or is limited by the tentative minimum tax (TMT), the unused credit can be carried over to the next six years or until it is exhausted, whichever comes first. It's important to apply the credit carryover to the earliest taxable year(s) possible, and no part of the credit can be applied against prior year taxes.

How are credits assigned to affiliated corporations, and what are the limitations?

Credits can be assigned to affiliated corporations according to Section 23685 of the Revenue & Taxation Code. Before a credit can be assigned, it must exceed the tax liability of the assignor for the taxable year when the credit is to be assigned. The election to assign any credit is irrevocable, and once assigned, it cannot be reassigned. Both the assignor and the eligible assignee should maintain records substantiating the credit assignment. Certain limitations apply, such as the inability to reduce tax liabilities below specific thresholds or to use the credit for purposes not allowed under the credit's provisions.

Common mistakes

Filling out the California 3541 form, which relates to the Motion Picture and Television Production Credit, requires careful attention to detail. Common errors can lead to processing delays or the rejection of the credit claim. Here are ten common mistakes:

- Incorrect identification numbers: Taxpayers sometimes enter the wrong Social Security Number (SSN), Individual Taxpayer Identification Number (ITIN), corporation number, or Federal Employer Identification Number (FEIN). Ensure these numbers match exactly as they appear on your tax return.

- Missing or incorrect Credit Certificate numbers: Each current year generated credit must be accompanied by its correct certificate number. Forgetting to include this number or inaccuracies can invalidate the credit claim.

- Omission of pass-through credit information: Taxpayers often neglect to attach a schedule showing details of credits received from pass-through entities, like the name and identification numbers of these entities, their credit certificate numbers, and the ownership percentage.

- Failure to specify the amount of credit purchased from other entities: This section is frequently overlooked or incorrectly filled out, leading to potential discrepancies in the total available credit.

- Incorrectly claiming credits assigned from affiliated corporations: Credits received through affiliations must be documented in Part III, yet this requirement is frequently disregarded.

- Not listing all Credit Certificate numbers for multiple credits: When reporting multiple current year generated credits, failing to list all applicable Credit Certificate numbers can lead to partial recognition of your total available credits.

- Incorrectly reported or omitted credit sales: The amount of credit sold to unrelated parties from Form FT office 3551 must be accurately reported; inaccuracies or omissions here can undermine the integrity of the claim.

- Confusion over credit application against sales and use taxes: Taxpayers sometimes mistakenly omit or inaccurately report the amount of credit applied towards qualified sales and use taxes.

- Miscalculation of Tax Liability: For corporations, ensuring that the tax liability is accurately reported in Part IV is critical. Errors in this calculation can affect the excess credit available for assignment to affiliated corporations.

- Incomplete details in the Assigned Credit from Affiliated Corporations sections: In both assigning and receiving credit, completeness and accuracy of information such as assignor and assignee names, their identifiers, and the assigned credit amount are crucial. Missing or incorrect entries can lead to unapproved credit assignments.

Attention to these areas when completing the California 3541 form can significantly improve the likelihood of approval for your Motion Picture and Television Production Credit claim.

Documents used along the form

When working with the California Form 3541, the California Motion Picture and Television Production Credit form, there are several other documents and forms that may be crucial throughout the process. Below is a list of documents often used alongside California Form 3541, each serving a unique role in ensuring compliance and optimization of benefits under the California tax code.

- Form FTB 3544: Election to Assign Credit Within Combined Reporting Group. This form is used by corporations to assign tax credits to affiliated corporations within a combined reporting group, facilitating the strategic utilization of tax credits across related entities.

- Form FTB 3544A: List of Assigned Credit Received and/or Claimed by Assignee. Accompanying Form FTB 3544, this form details the specifics of the credit assignments, including the amounts assigned and the receiving affiliates, ensuring transparency and compliance in credit allocation.

- Form FTB 3551: Sale of Credit Attributable to an Independent Film. This form is specific to the sale of tax credits generated from independent film productions, a unique provision that allows qualified taxpayers to monetize unused credits.

- Form M: Tax Credit Certificate. Issued by the California Film Commission, this certificate validates the amount of tax credit allocated to a taxpayer for qualified motion picture and television production expenditures.

- Form 540: California Resident Income Tax Return. Individual taxpayers attach Form 3541 to their annual tax return, either Form 540 for residents or the relevant form for nonresidents and part-year residents to apply their production credits against personal income tax.

- Form 100: California Corporation Franchise or Income Tax Return. Corporate taxpayers attach Form 3541 to this return to apply their motion picture and television production credits against their corporate tax liabilities.

- Form 100S: California S Corporation Franchise or Income Tax Return. S corporations use this form alongside Form 3541 when allocating and utilizing film and television tax credits through the S corporation tax structure.

- Form 568: Limited Liability Company Return of Income. For LLCs taxed as partnerships, this form would be used in conjunction with Form 3541 to report and pass through production credits to the members.

- Board of Equalization Filings: While not a single form, dealings with the California Board of Equalization may involve multiple documents for taxpayers electing to apply motion picture credits against sales and use tax liabilities.

Understanding and utilizing these documents effectively can be critical for taxpayers seeking to maximize the benefits of California's motion picture and television production credit. Each document plays a role in the broader context of tax planning and compliance for qualified productions, spanning from the initial allocation of credits by the California Film Commission to the actual application of those credits against income or sales and use tax liabilities. Whether working within a corporate structure or as an independent filmmaker, being familiar with these forms ensures that taxpayers can navigate the complexities of California's incentive program efficiently.

Similar forms

The California Form 3541, related to the Motion Picture and Television Production Credit, is comparable to several other types of tax documents that also facilitate tax incentives for specific activities or industries. These documents, while unique to their purposes, share structural and procedural similarities with Form 3541, offering insights into how tax credits can be utilized, tracked, and reported.

One similar document is the New York State Film Production Credit application form. Like California's Form 3541, this form is designed for entities in the film and television production industry, aiming to incentivize productions through tax credits. Both forms require detailed information about the production expenditures and have provisions for transferring or assigning credits, demonstrating the states’ efforts to attract and retain film production activities.

The Federal Form 3468, Investment Credit, is another document that shares similarities with Form 3541. Although it pertains to a broader range of industries and investments, including renewable energy and historic preservation, it involves the allocation of tax credits to incentivize certain activities. Both forms require the taxpayer to calculate and substantiate the credit amount, reflecting their contribution to specified economic activities.

The California Form 3800, General Business Credit, also resembles Form 3541 in its function of reporting various business-related tax credits. Taxpayers can use Form 3800 to claim different credits, including those for research and development or environmental conservation, mirroring the way Form 3541 is used specifically within the motion picture and television production industry for similar tax advantage purposes.

Similarly, the Texas Moving Image Industry Incentive Program (TMIIIP) application captures the essence of promoting film, television, commercial, and video game productions through financial incentives. Like California's Form 3541, it seeks to provide a boost to local productions through tax credits or rebates, requiring detailed documentation of production expenditures and activities within the state.

The California Form 3523, Research Credit, is geared towards businesses investing in research and development within the state. Although targeting a different sector, it parallels Form 3541 in allowing businesses to claim tax credits against income or franchise taxes, emphasizing the state's support for growth in various innovative and creative sectors, including entertainment and technology.

Another document, the Louisiana Motion Picture Investor Tax Credit application, offers incentives to attract film productions to the state. Like California's Form 3541, Louisiana's program allows for the sale or transfer of tax credits, highlighting the flexible nature of tax incentives in stimulating economic activities in targeted industries.

Lastly, the Federal Historic Preservation Tax Incentives application form, while focused on real estate and historic preservation, shares a fundamental goal with Form 3541: encouraging specific investments through tax credits. Both forms require applicants to provide detailed accounts of their projects to qualify for the tax benefits, illustrating the government's role in guiding investment toward desired outcomes.

Dos and Don'ts

When navigating the complexities of the California Form 3541 for Motion Picture and Television Production Credit, attention to detail can make a significant difference. Here are ten dos and don'ts that can help streamline the process and avoid common pitfalls:

- Do thoroughly review the form instructions provided by the Franchise Tax Board to understand eligibility criteria and documentation requirements.

- Do not skim over the instructions. Every line and requirement can impact your tax situation and the amount of credit you can claim.

- Do gather and organize all necessary documentation related to qualified production expenditures before starting the form to ensure a smooth process.

- Do not estimate or guess amounts. Precise figures are necessary to calculate your available credit accurately.

- Do write the credit certificate number clearly and correctly on line 1b, as this links your form to the credit allocation from the California Film Commission.

- Do not ignore the importance of the credit certificate number. It is a crucial piece of information that validates your credit claim.

- Do correctly calculate the total available credit on line 6 by carefully adding the relevant amounts from lines 1a, 2, 3, 4, and 5.

- Do not forget to subtract the sum of lines 7, 8, and 9 from line 6 when determining your total available credit on line 10. This step is vital for an accurate credit claim.

- Do ensure that any assigned credits from affiliated corporations are properly reported in Part III and that the assignor's details are accurately filled out.

- Do not hesitate to seek clarification on specific lines or instructions from a tax professional if you encounter difficulties or have questions about the form.

By following these guidelines, you can avoid common mistakes and ensure that the process of claiming your California Motion Picture and Television Production Credit is as accurate and efficient as possible.

Misconceptions

Understanding the California 3541 form, associated with motion picture and television production credits, can be confusing. Several misconceptions surround its use and application. Here, some of the most common misunderstandings are clarified.

- The form is only for big Hollywood productions. While it's true that major motion picture and TV productions can benefit from this credit, smaller independent films and relocated TV series also qualify, as long as they meet the budget requirements outlined by the state.

- Any production expense qualifies for the credit. Not all expenses incurred during production qualify for the credit. Only those identified as "qualified expenditures" under the specific criteria set by the California Film Commission are eligible.

- The credit is refundable. This credit is not refundable. If the credit amount exceeds the tax liability, the remaining balance can be carried forward for future tax years but cannot be refunded.

- Credits can be freely transferred between entities. Although credits can be sold or assigned, there are specific rules governing these transactions. For instance, only independent film credits may be sold, and only certain entities can engage in the sale or assignment of credits.

- Any California tax form can be used to claim the credit. Taxpayers need to attach the completed Form 3541 to their California tax return, indicating this on the form by writing “CFC Credit” in red ink at the top margin. This is a specific requirement for claiming the motion picture and television production credit.

- The credit amount is based on total production costs. The credit amount is actually calculated as a percentage of qualified expenditures, not the total production cost. The rate is fixed at 20% for most productions, with some exceptions like independent films and TV series that relocate to California, which can receive 25%.

- Productions can claim the credit any time. To claim the credit, productions must first receive an allocation and certification from the California Film Commission. The application and allocation process follows a specific schedule and requirements that need to be met timely.

- The credit can be claimed by any taxpayer involved in the production. Only the entity that has been issued the credit certificate by the California Film Commission can claim the credit. However, this entity can pass the credit through to its shareholders, beneficiaries, partners, or members if it operates as a S corporation, partnership, LLC, or trust.

- There is no limitation to credit carryovers. Unused credits can be carried over to subsequent years but are subject to a six-year limitation. Credits cannot be applied retroactively to previous tax years.

- The entire credit must be used in the year it is claimed. If a taxpayer's credit amount exceeds their tax liability, or if applying the credit would result in their tax dropping below the tentative minimum tax (TMT), the excess can be carried over to future tax years, ensuring no benefit is lost.

Understanding these aspects of the California 3541 form helps ensure that eligible productions can effectively plan for and benefit from the available credits. It's crucial for filmmakers and production companies to carefully review the eligibility requirements and restrictions to maximize their benefits under this program.

Key takeaways

- California Form 3541 is designed to report motion picture and television production credits.

- Eligible taxpayers can use the credit to offset income or franchise tax liability, sell it (for independent films only), assign it to an affiliated corporation, or apply it against qualified sales and use taxes.

- The credit is non-refundable but can be carried over for six years or until exhausted, whichever occurs first.

- To claim a current year generated credit, the credit certificate number from the California Film Commission (CFC) must be provided on the form.

- Credits can be acquired through various means, including allocation by the CFC, pass-through from S corporations, trusts, partnerships, or LLCs taxed as partnerships, purchase from another entity, or assignment from an affiliated corporation.

- Credit limitations include restrictions on reducing certain taxes and charges, including the S corporation tax, the minimum franchise tax, and the alternative minimum tax.

- For corporations, the credit cannot reduce tax liabilities below the tentative minimum tax.

- In cases of sold credits attributable to an independent film, the seller must report the gain from the sale, whereas the buyer must report as income the difference between the purchase price and the credit amount claimed.

- Credit assignments to affiliated corporations are irrevocable, and both the assignor and assignee are liable for any resulting tax adjustments.

- Affiliated corporations eligible for credit assignments include those with 100 percent mutual ownership of voting common stock, as well as stapled entities as defined by tax codes.

- Documentation is crucial for substantiating the credit and its allocation, assignment, sale, or application against taxes; failure to properly document may lead to disallowance.

Discover More PDFs

How to File a Mechanics Lien - While a powerful tool, it's important for filers to act within the specified legal timelines to preserve their lien rights.

California Gun Permit - Recognize the importance of providing a social security number for tax enforcement and compliance with family support judgments in your gun permit application.

Pre Lien Form - The distribution of this notice helps minimize the risk of financial loss for those providing services or materials, encouraging a more reliable and virtuous construction market.